EUR/USD attracts some buyers amid the risk-on mood.

ADP private payrolls came in worse than expected, rising 103K in November vs. 106K prior.

Eurozone Retail Sales rose 0.1% MoM in October vs -0.1% prior, below the market consensus of 0.2%.

The Eurozone GDP for Q3 and US Jobless Claims will be the highlights on Thursday.

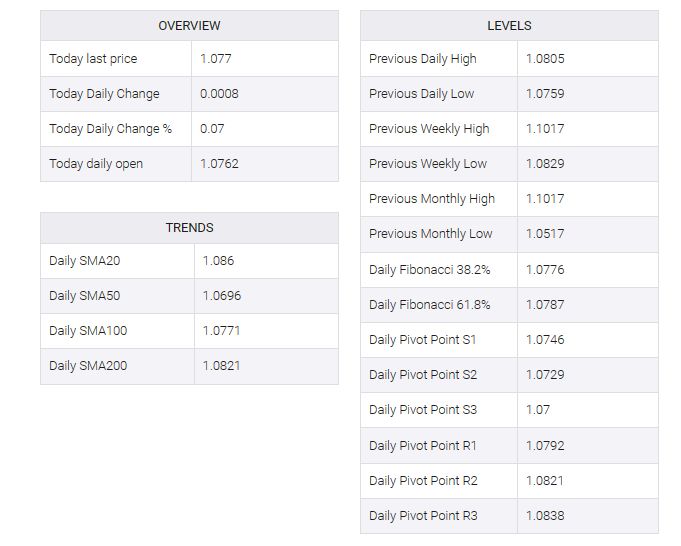

The EUR/USD pair posted modest gains in the early Asian session on Thursday. However, the pair’s upside may be capped on renewed US dollar (USD) demand and expected-less Eurozone data. The major pair is currently trading near 1.0770, up 0.08% on the day.

The US Dollar Index (DXY) rose for three straight days despite weak ADP employment data. On Wednesday, ADP private payrolls rose to 103K in November from 106K in October. These figures came in worse than expected. Market players will take further cues from US employment data this week, including weekly jobless claims and nonfarm payrolls.

Weaker eurozone retail sales exert some selling pressure on the euro (EUR). The figure rose 0.1% MoM in October vs -0.1% in September, below the market consensus of 0.2%. On an annual basis, eurozone retail sales fell to 1.2% from 2.9% in October, worse than expected for a 1.1% drop. High interest rates, weak consumer confidence, and subdued optimism about the labor market all combined to dampen growth in private consumption.

ECB board member Isabelle Schnabel said last month that rate hikes must remain an option as the last phase of the fight against inflation could be the toughest. However, he changed his stance after three surprisingly low inflation readings in a row. Markets are aggressively pricing the European Central Bank (ECB) to cut interest rates by 142 basis points (bps), with the first move now seen in March 2024.

Looking ahead, investors await the Eurozone’s Gross Domestic Product for the third quarter (Q3), which is projected to be flat at -0.1% QoQ. In the US docket, weekly unemployment claims are due

EUR/USD